Dave is a marketing expert with 15 years experience in the tech and SaaS world. He specializes in educating IT and channel audiences, with a focus on security, privacy, compliance, and marketing technology. With a talent for storytelling and a deep understanding of the industry, Dave transforms complex IT topics into clear, engaging, and impactful narratives.

The hidden compliance gaps in your financial firm's email communications

It’s 11:30pm. A regulator just flagged a missing disclosure in a routine client email. Your team is trying to track down the sender, find the message, and work out where it broke.

The root cause? An email signature that wasn’t updated.

For many financial services IT teams, this kind of scenario isn’t rare. It happens when systems don’t talk to each other, when controls are inconsistent, and when ownership of email content slips between teams.

Most organizations focus on the obvious parts of email compliance like encryption and archiving. But issues often start earlier, in the everyday elements that go unnoticed. Disclaimers that aren’t applied. Job titles that are out of date. Email signatures that look different from team to team.

When these pieces aren’t aligned, they create risk. And when something fails, IT is expected to fix it.

This post explores the compliance gaps that are hiding in plain sight. It looks at how overlooked details in your email environment can lead to audit issues, regulatory fines, and time-wasting cleanup work—and what you can do to prevent it..

The rising cost of non-compliant communications

Financial institutions are under pressure. Regulations are evolving fast. Enforcement is ramping up.

In the last 12 months, more than $2.5 billion in fines have been issued by the SEC, FINRA, and CFPB for communications and recordkeeping violations. Regulators expect organizations to control how they communicate—across every message, channel, and team.

In the last 12 months, more than $2.5 billion in fines have been issued by the SEC, FINRA, and CFPB for communications and recordkeeping violations. Regulators expect organizations to control how they communicate—across every message, channel, and team.

Frameworks like Basel III now treat poor communication governance as an operational risk. And new mandates like MiCA, PSD3, and AMLA introduce disclosure requirements that go beyond product documentation. Email formatting, disclaimers, and auditability are all in scope.

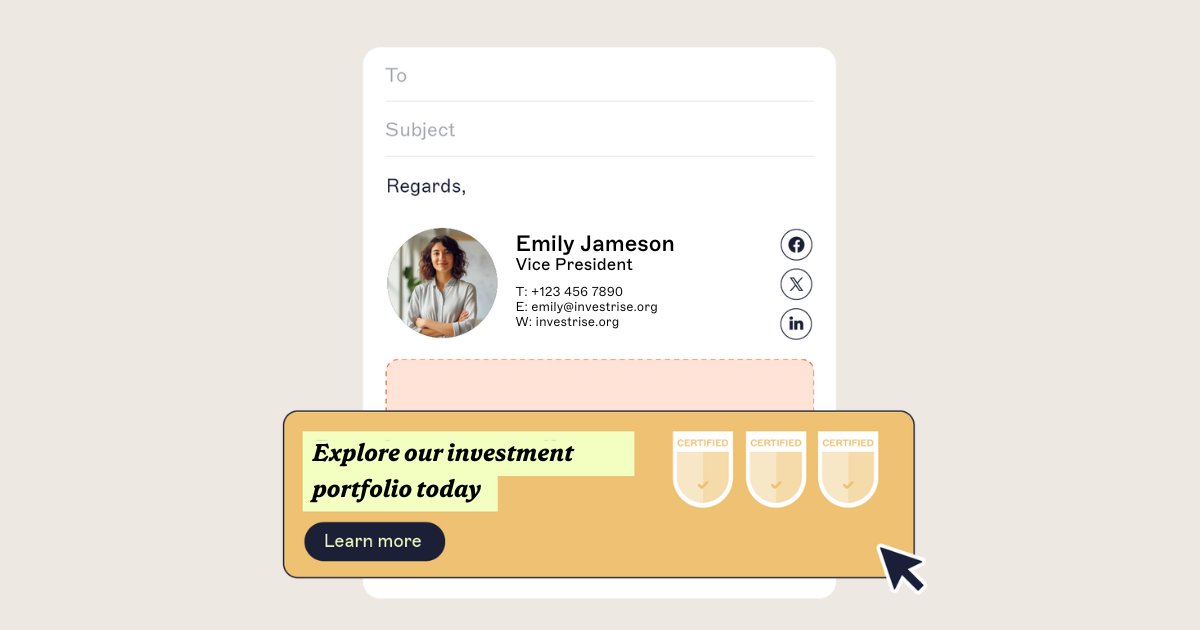

This level of scrutiny affects how financial services companies manage day-to-day communication, including their email signatures.

When credentials are inconsistent, disclaimers are missing, or formatting varies by team, it introduces risk. It makes it harder to prove internal controls. And it creates audit gaps that compliance teams must answer for.

Every new regulation brings more than policy updates. IT teams also have to figure out how to apply those changes across thousands of daily emails—without turning it into a manual task list.

Email compliance requirements for financial services organizations

The financial services industry is tightly regulated to prevent fraud, protect data, and ensure fair practices, fostering market stability and client trust.

Below are some of the most important regulations and their connection to email disclaimers. Click on the arrows to learn more:

Below are some of the most important regulations and their connection to email disclaimers. Click on the arrows to learn more:

1. General Data Protection Regulation (GDPR) – EU

The General Data Protection Regulation (GDPR) is the strongest privacy and security law in the world. It governs how organizations both within and outside the EU collect, process, and protect the personal data of EU residents, while at rest and in transit.

This is especially critical in financial services, where firms handle large volumes of sensitive personal and financial information.

The disclaimers within your email signatures support GDPR compliance by:

Informs clients about confidentiality and security

Communicates data usage practices clearly

Reinforces trust through transparent handling of personal information

2. California Consumer Privacy Act (CCPA) – U.S.

The California Consumer Privacy Act (CCPA) emphasizes consumer data protection and transparency, requiring organizations to disclose how they collect, use, and share personal information.

Adding a data privacy disclaimer to email signatures helps financial firms comply with CCPA regulations by reinforcing responsible data handling practices and building client trust.

Reinforces privacy statements in direct communications

Demonstrates transparency to regulators and clients

3. Securities and Exchange Commission (SEC) – U.S.

The Securities and Exchange Commission (SEC) enforces regulations governing financial services firms, including requirements for email communications under Rule 17a-4, which mandates email archiving for regulatory review.

To comply with SEC rules, many firms include disclaimers stating that:

Email messages may be monitored and stored

Financial advice or analysis is subject to regulatory review

4. The Financial Industry Regulatory Authority (FINRA) – U.S.

The Financial Industry Regulatory Authority (FINRA) is a U.S. self-regulatory organization overseeing the securities industry. It enforces rules to ensure brokers follow ethical practices, promoting trust and transparency in financial services.

Email disclaimers can help align with FINRA’s Rule 2210 by:

Standardizes disclosures across client-facing teams

Reduces the risk of omitted legal content

Supports fair, balanced investor communication

5. Sarbanes-Oxley Act (SOX) – U.S.

The Sarbanes-Oxley Act (SOX) promotes transparency in financial reporting and protects against fraud. Section 404 mandates annual reports on internal controls. For compliance, financial institutions implement measures like accurate record-keeping and fraud prevention.

Many include email disclaimers stating:

Emails may be recorded and audited for transparency

Demonstrates accountability in communications

6. Gramm-Leach-Bliley Act (GLBA) – U.S.

The Gramm-Leach-Bliley Act (GLBA) is a U.S. federal law protecting consumers' personal information held by financial institutions. A key component is the Safeguards Rule, which requires institutions to implement security plans to mitigate risks to customer data.

Email disclaimers support GLBA compliance by:

Advises clients not to share personal data via email

Reinforces the institution’s data protection policy

7. Financial Conduct Authority (FCA) – UK

The Financial Conduct Authority (FCA) regulates UK financial services, ensuring firms follow rules, protect consumers, and uphold market integrity. Firms must communicate clearly, fairly, and transparently with clients while keeping records of all interactions, including emails.

Email disclaimers support FCA compliance by:

Creating a clear audit trail for client communications

Helping firms meet regulatory standards effectively

Emerging compliance requirements to monitor

1. Markets in Crypto Assets Regulation (MiCA) – EU

Email signatures support Markets in Crypto Assets Regulation (MiCA) compliance by embedding disclaimers and legal identifiers that meet jurisdictional requirements.

2. Anti-Money Laundering Authority (AMLA) – EU

Centralized email signature management allows financial firms to control and customize legal messaging for high-risk departments like KYC and compliance.

3. Payment Services Directive 3 (PSD3) – EU

Email signatures help communicate updates to customer rights, terms, and security policies across jurisdictions.

4. Digital Operational Resilience Act (DORA) – EU

Signature platforms that provide consistent, logged communications support Digital Operational Resilience Act's (DORA) requirements for communications oversight and operational control.

5. Basel III Final Reforms – Global

Centralized email signature management demonstrates maturity in risk oversight and strengthens internal messaging governance when it comes to Basel III.

The financial, legal, and reputational risks of non-compliance

Poor email signature management in financial services can have far-reaching consequences.

Beyond regulatory fines, organizations may face lawsuits, operational disruptions, and lasting damage to their reputation.

Beyond regulatory fines, organizations may face lawsuits, operational disruptions, and lasting damage to their reputation.

Fines for non-compliance: Failure to comply with financial services regulations can lead to significant penalties. For example:

GDPR violations: Fines of up to €20 million or 4% of global revenue.

CCPA violations: Californian residents can sue companies for damages ranging from $100 to $750 per individual.

FINRA violations: Fines of up to $1 million per rule violation, plus potential restitution payments.

Legal exposure and trust breakdown: If an email includes inaccurate credentials or omits mandatory disclosures, it creates risk:

Clients may misinterpret information

Legal teams may be forced to respond to disputes

Reputational damage can undermine long-term client relationships

Reputational damage: Financial services firms operate in an industry where trust is paramount. Inconsistent or missing email disclaimers can:

Signal carelessness in compliance efforts

Raise concerns about transparency and security

Lead to long-term reputational harm that is difficult to repair.

Operational inefficiencies: IT teams rarely have the time or capacity to manage email signature updates across departments. When something breaks, they’re the ones rewriting policies, adjusting settings, and chasing teams to fix it. Challenges include:

IT resource overload: Constant compliance updates across departments consume unnecessary IT hours.

Error correction: Addressing compliance violations after they occur is far more expensive than proactive management.

Scalability issues: Without centralized control, growth becomes challenging, as each new hire requires manual intervention.

Compliance frameworks that impact email signatures in financial services

To better understand the impact of non-compliance, let's explore real-life examples where organizations failed to meet regulatory requirements and what the consequences were.

1. Four Banks fined £104.5 million for sharing sensitive information

In February 2025, the UK's CMA fined Citigroup, HSBC, Morgan Stanley, and RBC £104.5 million ($132.4 million) for illegally sharing sensitive UK government bond information between 2009 and 2013 via emails and chatrooms.

Unauthorized or inconsistent use of email signatures can complicate the monitoring and auditing of communications. This then makes it challenging to attribute messages to specific individuals and increases the risk of non-compliance.

2. Robinhood Markets, Inc. – $45 million fine for record-keeping failures

In January 2025, Robinhood Markets agreed to pay $45 million to the SEC for securities law violations, split between Robinhood Securities ($33.5M) and Robinhood Financial ($11.5M). Violations included improper recording of fractional share trades and a 2021 data breach exposing customer data. The SEC cited inadequate policies to protect customer information and prevent identity theft.

Misleading or inaccurate job titles or certifications in email signatures can contribute to data protection breaches and regulatory penalties.

3. ABN AMRO – €480 million fine for anti-money laundering (AML) failures

In April 2021, ABN AMRO Bank N.V. agreed to pay €480 million to settle with the Netherlands Public Prosecution Service over serious anti-money laundering shortcomings between 2014 and 2020. The bank failed to properly monitor client activities and report suspicious transactions.

Neglecting to include confidentiality notices in email signatures can lead to unauthorized sharing of sensitive information, increasing compliance risks.

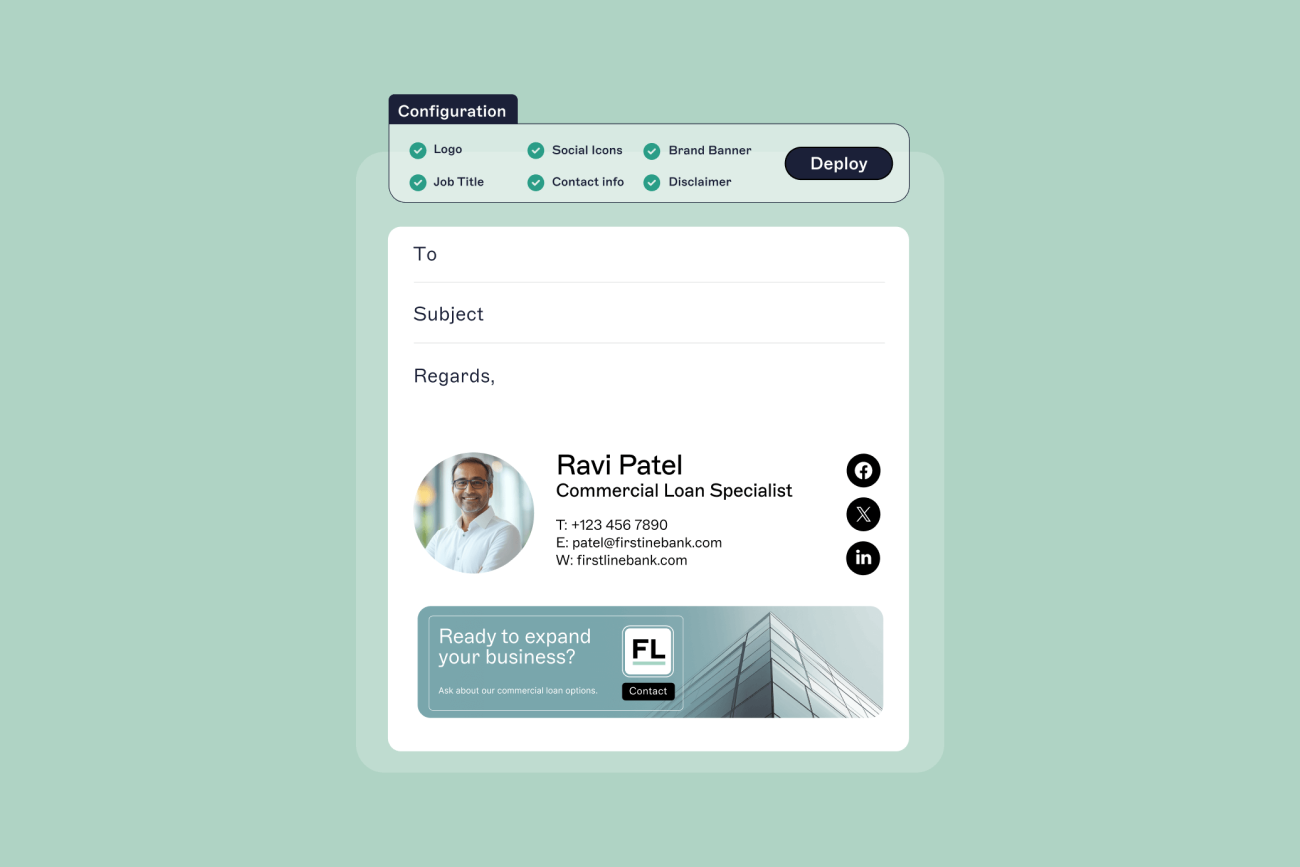

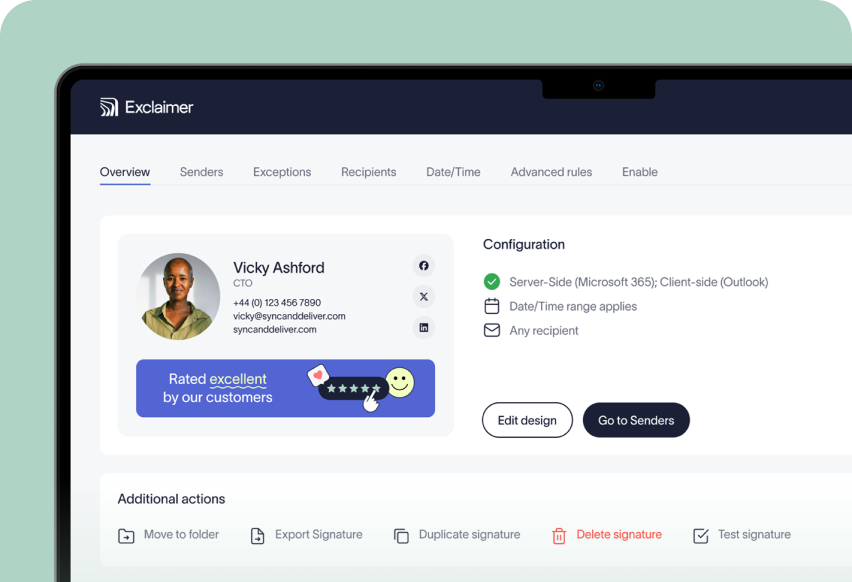

How centralized email signature management protects against regulatory risks

Manually managing email signatures in a financial organization is inefficient and risky. Centralized email signature management ensures compliance, consistency, and professionalism—without employee effort.

The key benefits of centralized email signature management for financial services firms include:

The key benefits of centralized email signature management for financial services firms include:

Ensure compliance with ease: A centralized system lets financial institutions update email disclaimers in real-time, adapting to regulations without requiring manual updates, reducing compliance risks.

Maintain consistency and professionalism: Standardized email signatures ensure consistent branding, messaging, and professionalism across the organization.

Save time and reduce errors: Automating email signature updates eliminates manual configuration, reducing errors and freeing IT resources for strategic tasks.

Boost security and compliance: Consistent email disclaimers help financial firms protect client data, avoid penalties, and simplify audits.

Strengthen reputation and efficiency: A strong email signature strategy builds credibility while centralized management simplifies compliance and operations.

IT teams want more than compliance. They want fewer late-night calls, less back-and-forth with legal, and fewer gaps to fix after audits. Centralized email signature management helps fix a critical part of the compliance equation. But it's only one part.

A practical tool for financial services audit readiness

To fully assess risk, financial institutions need visibility across the entire email environment, not just how messages are signed off.

That means evaluating:

Whether legal disclaimers are accurate and applied consistently

How email communications are controlled, monitored, and archived

If branding aligns with compliance expectations across teams

Whether processes reflect the requirements of GDPR, MiCA, PSD3, AMLA, Basel III, and other frameworks

We’ve created a self-audit checklist to help IT and compliance leaders identify gaps, reduce exposure, and prepare for regulatory scrutiny.

Use it to benchmark your communications setup against the compliance expectations that matter most.

👉 Download the Email Compliance Checklist